Preliminary Results

Preliminary Results for April 2026

April 2026

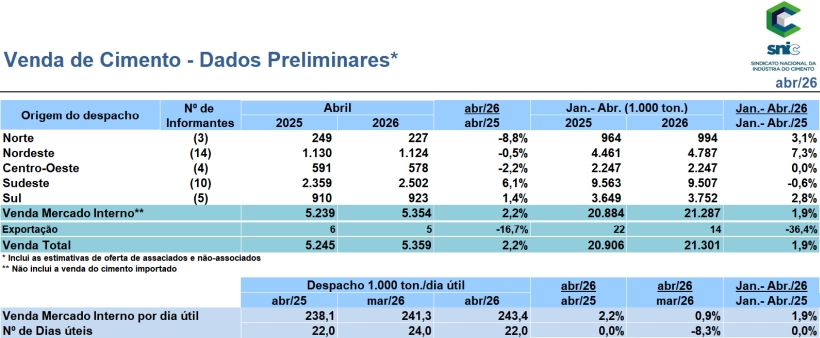

Cement sales in April 2026 totaled 5.4 million tons, registering a 2.2% increase compared to the same month in 2025, according to the National Cement Industry Union (SNIC). In the first four months of the year, the sector showed a growth of 1.9% compared to last year.

The volume of cement sales per working day reached 243,400 tons, a 0.9% increase compared to March and a 2.2% increase compared to the same month in 2025. In the accumulated year (Jan-Apr), the performance shows a growth of 1.9%.

The economic outlook that sustains demand continues to be influenced by the heated labor market. The unemployment rate in the first quarter closed at 6.1%, the lowest level for the period since 2012, keeping the wage bill at its highest historical level. This scenario, coupled with the income tax exemption, has led to a rise in consumer confidence¹ for the second consecutive time this year, with particular emphasis on the improved perception of the financial situation among lower-income families.

The real estate market also acts as an important driver of growth for the sector. Sales and launches continue to rise, driven mainly by the Minha Casa, Minha Vida (MCMV) program, which already accounts for 52% of real estate launches. In the accumulated period up to March 2026, the number of financed units jumped 149%, correcting the sharp decline of last year.

Adjustments to the MCMV have broadened access for the middle class to larger and better-located properties, raising the income ceiling and the value of the units. All this movement is supported by a new contribution, announced in April, of R$ 20 billion from the pre-salt reserves, which allowed the government to raise the contracting target to 3 million homes, from 2023 until the end of 2026.

In parallel, recent updates to housing programs have altered credit prospects for the sector. The limit for the home renovation program increased from R$ 30,000 to R$ 50,000, with a unified interest rate of 0.99% per month and an expanded public with family income up to R$ 13,000.

Despite good prospects in housing, the macroeconomic environment inspires caution. Construction confidence² fell in April. The same movement was observed in the perception of industry³, which fell for the first time in the last five months, reflecting a less heated environment and slightly above-normal inventories.

In addition to the difficulty in attracting labor, the impacts of the war in the Middle East were decisive for the pessimism of these indicators. International instability has raised inflation expectations for 2026, directly impacting projections for the Selic rate. The market predicted the year would end at 12%, but now projects 13%, a direct reflection of the pressure from oil prices, freight costs in production, and exchange rate volatility.

There are also significant obstacles to consumption and credit. Indebtedness has reached a record level, compromising 49.9% of the population's income, and default affects 82.8 million Brazilians. The accelerated growth of online betting has subtracted R$ 143.8 billion from commerce in the last two years and has led thousands of families into default, consuming part of the resources previously directed towards construction.

The sector still views the guidelines of the New Desenrola program with apprehension. The program foresees the use of resources from the Severance Indemnity Fund (FGTS) to pay off family debts, deviating from the fund's main function, which was structurally created to finance the acquisition of real estate. This measure diverts, once again, essential resources and threatens the sustainability of the main funding for housing credit in the country.

“Despite the positive results in cement sales so far, the activity is already feeling the effects of the conflict in the Middle East. We had a strong impact with the readjustment in petroleum coke, a component that is mostly imported, which accounts for about 40% of the production cost. In addition, significant increases in inputs from abroad, such as explosives, ammonia, urea, cement additives and maritime freight itself, have registered a sharp increase. In the domestic market, pressures persist with the readjustments of diesel oil and road freight, a mode that represents about 90% of cement distribution in the country.” Paulo Camillo Penna – President of SNIC