Preliminary Results

Preliminary Results for May 2026

May 2026

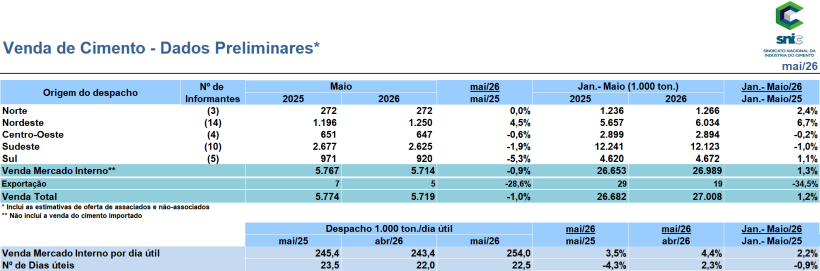

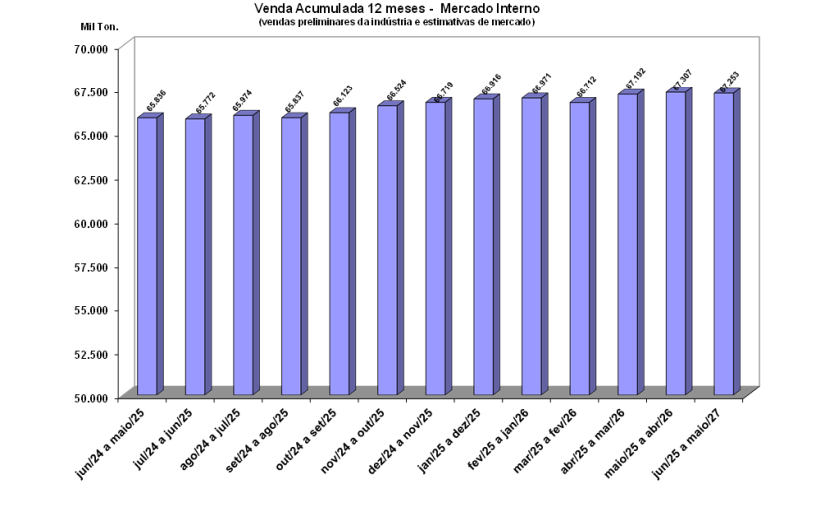

Cement sales in May 2026 totaled 5.7 million tons, registering a 1.0% drop compared to the same month in 2025, according to the National Cement Industry Union (SNIC). In the accumulated total for the first five months of the year, the sector showed a growth of 1.2% compared to last year. The volume of cement sales per working day, a key performance indicator, registered 254,000 tons, an increase of 4.4% compared to April and 3.5% compared to the same month in 2025. In the accumulated total for the year (Jan-May), the performance shows an increase of 2.2%.

The result continues to be supported by the heated labor market and the real estate market, strongly driven by the Minha Casa, Minha Vida (MCMV) program. In addition, the acceleration of road projects with rigid pavement, combined with the development of technologies for the implementation of concrete streets and avenues, has been an important driver of cement demand. Despite resilient sales, the industry faces a challenging scenario of high interest rates (Selic), inflation, and strong cost pressures generated by instability in the Middle East.

The national economic situation reflects this performance. The unemployment rate closed at 5.8% in April, the lowest level for the month since 2012, keeping the wage bill stable and close to its highest historical level, even with a slight drop in income. Despite this positive scenario, consumer confidence¹ fell in May, reflecting an adjustment after two months of increases, with lower-income families signaling a worse outlook for the future. The informality rate remained stable at 37.2%. On the other hand, the generation of formal jobs disappointed and raised an alert, registering the worst result for the month of April since 2021.

In the real estate market, sales rose 4.1% in the first quarter, driven by the MCMV (Minha Casa Minha Vida program), which recorded a 10% jump in the period and already represents 49% of the sector's launches. The R$20 billion investment from pre-salt oil reserves allowed the government to raise its target to 3 million contracted homes by the end of 2026. In parallel, the home renovation program was also expanded, with an increase in credit to R$50,000 and a reduction in the interest rate to 0.99% per month.

The macroeconomic scenario continues to inspire caution. Inflation expectations continue to rise and, coupled with external uncertainties and oil costs, have led the market to raise its projection for the Selic rate at the end of the year to 13.50%. Confidence in the construction sector² remained stable in May, although the building segment showed more pessimism in the face of labor shortages and cost pressures. Meanwhile, industrial confidence³ grew again in May, driven by improved demand and the normalization of inventories after the initial shock from the war in the Middle East, although the environment remains uncertain and vulnerable to disruptions in the production chain.

In the retail sector, the scenario is also one of contraction. In April, sales of construction materials fell by 4.9%. This drop highlights a persistent bottleneck: the restriction on consumption and credit. With debt compromising 49.8% of family income, default has hit a historic record and now affects 83.3 million Brazilians. This situation has been aggravated by the accelerated growth of online betting, which has subtracted R$ 143.8 billion from retail trade in the last two years and dragged 269,000 families into default.

Finally, the sector remains apprehensive about the guidelines of the New Desenrola program, which continues to encourage the use of FGTS (Brazilian employee severance fund) resources to pay off debts. The measure highlights the deviation from the fund's primary function, which was structurally created to finance access to housing.

“The sector is experiencing mixed signals. On the one hand, it is undeniable that the strengthening of the labor market and updates to housing programs are cornerstones for positive results. However, we are dealing with a negative scenario of a smaller drop in the Selic rate and high inflation, accentuated by instability in the Middle East. Furthermore, the industry is closely monitoring the vote on the bill that proposes ending the 6x1 work schedule, since this possible labor change has the potential to significantly increase the industry's operating costs.” Paulo Camillo Penna – President of SNIC