Preliminary Results

Preliminary Results for June 2026

June 2026

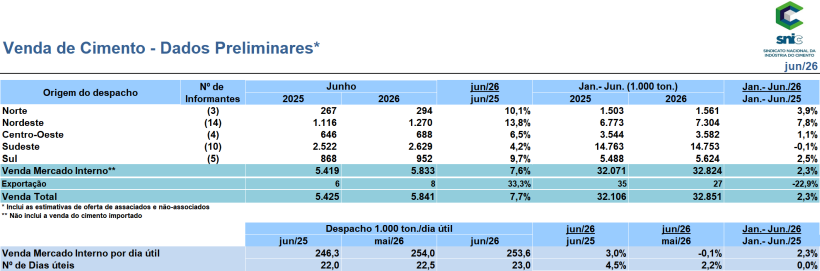

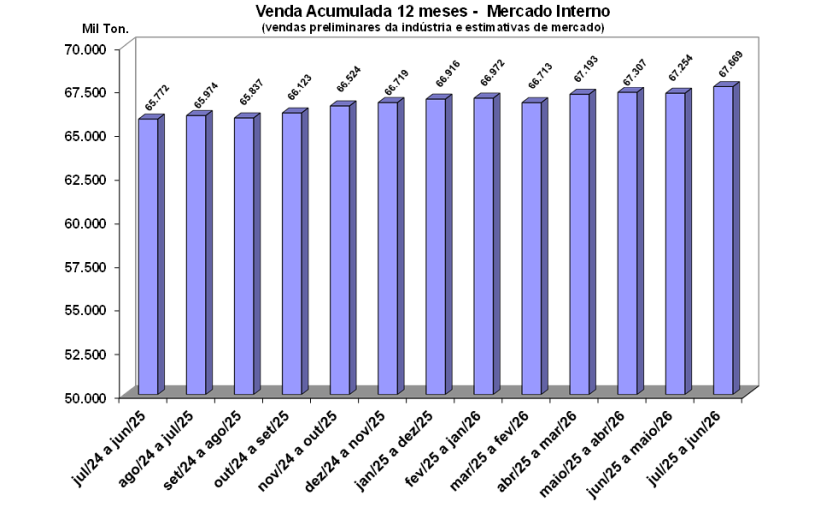

Cement sales in Brazil rose by 2.3% in the first half of 2026 compared to the same period last year, totaling 32.9 million tonnes. In June alone, 5.8 million tonnes were sold—a 7.7% increase over 2025—according to the National Cement Industry Union (SNIC). Shipments per working day averaged 253.6 thousand tonnes, representing a 3.0% increase compared to June of the previous year and a 0.1% decline relative to May.

The semester's positive performance was driven by a robust labor market; unemployment closed the quarter ending in May at 5.6%—the lowest rate for the period since 2012—and the employed population reached a historic high of 102.7 million people, keeping the total wage bill at a high level.

In the real estate market, the *Minha Casa, Minha Vida* (MCMV) program remains the primary sales driver, accounting for 50% of new real estate launches in the first quarter of the year and recording a 10% rise in sales. The inclusion of the middle class in the program (Tier 4) starting in April, combined with the government's revised target of 3 million housing units by the end of 2026, has the potential to generate an additional 5 million tonnes in cement consumption.

At the same time, the infrastructure sector is opening up new demand prospects through the acceleration of rigid concrete pavement (whitetopping) road projects. This technology is establishing itself as a solution that is more cost-effective, durable, and aligned with the Ministry of Transport's new emissions reduction guidelines.

Despite these advances, the sector is facing a sharp rise in operating costs. In the international market, ocean freight and petroleum coke saw price increases of around 30% in 2026. Domestically, rising diesel prices drove up road freight costs by 25%, and a potential shift to a 5x2 work schedule (40-hour week) is estimated to raise labor costs by approximately 15%. Cement manufacturing operations run 24 hours a day, 365 days a year.

The credit and income landscape also raises red flags. Projections that the Selic rate will end the year at 14%—slowing the pace of rate cuts—increase the cost of housing finance and heighten competition between financial assets and real estate investments.

Added to this is the impact on household budgets caused by the rise of online betting platforms, which have diverted R$ 143.8 billion away from retail spending over the past two years and pushed 269,000 families into default, directly competing with funds previously earmarked for self-built housing and renovations. For over two years, the cement industry has been warning about the worsening debt and default levels fueled by online betting, yet there has been no corresponding government action to curb the practice. The sector is also concerned about the diversion of FGTS funds from their core purpose (financing real estate) toward settling debts under programs like "Novo Desenrola."

Against this backdrop, expectations at the end of the half-year were mixed. Consumer confidence¹ remained stable, supported by employment levels and debt renegotiations, while industrial confidence² improved, reflecting the easing of Middle East conflicts and the stabilization of international oil prices. Conversely, the construction sector³ showed signs of pessimism, weighed down by rising costs, slowing activity, and a severe shortage of skilled labor. Regarding the environmental agenda, energy transition and decarbonization initiatives continue to advance steadily. Co-processing—a technology implemented by the cement industry utilizing materials ranging from biomass and industrial waste to Refuse-Derived Fuel (RDF)—has already achieved a thermal substitution rate of approximately 30% through the use of 3 million tons of waste. This volume is equivalent to one and a half times the annual waste generated by a city like Rio de Janeiro, while also preventing the emission of approximately 2.8 million tons of CO₂ into the atmosphere.

The Net Zero 2050 Roadmap, launched at COP30, continues to progress across key pillars such as alternative raw materials and fuels, energy efficiency, Nature-based Solutions (NbS), and carbon capture and utilization. Simultaneously, the sector is collaborating with the Ministry of Finance—through the Special Secretariat for the Carbon Market—on the structuring and regulation of the Brazilian Emissions Trading System (SBCE).

“The sector closes the first half of the year with a positive performance. Declining unemployment and a total wage bill at historic levels were key factors in this outcome. Housing—particularly the Minha Casa, Minha Vida program—combined with the acceleration of rigid-pavement road projects and concrete roadways, played a decisive role in our growth.

The economic landscape calls for caution: rising inflation, upward revisions to interest rate (Selic) projections, and record levels of household debt continue to severely constrain credit capacity and consumer spending. Nevertheless, the sector maintains its outlook of ending the year with growth of close to 2%.”

José Eduardo Ramos, President of Cimento Nacional and Chairman of the Board of SNIC/ABCP